Property insurance is a financial protection policy that safeguards your physical property—such as a house, apartment, commercial building, or industrial unit—against financial loss caused by unexpected events like fire, natural disasters, theft, vandalism, or accidents. It ensures that the owner does not bear the full financial burden when property damage or loss occurs. In India, property insurance policies are regulated by the Insurance Regulatory and Development Authority of India (IRDAI), which governs policy structure, insurer practices, claim settlement standards, and consumer protection.

1. What Does Property Insurance Mean in Simple Terms?

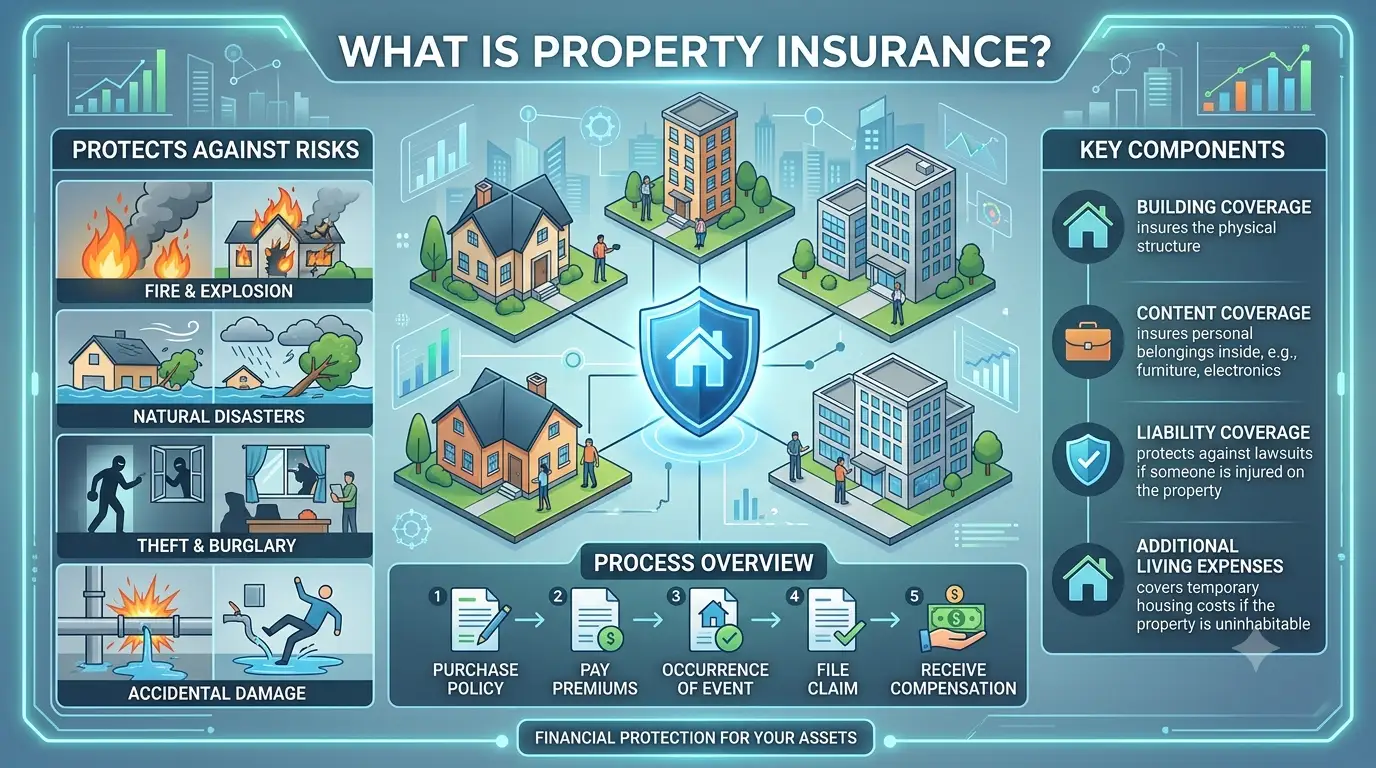

Property insurance is a risk-transfer mechanism.

- You pay a premium to an insurance company

- The insurer promises to financially compensate you

- Compensation applies if your property is damaged due to covered risks

It protects the structure, contents, or business assets depending on the policy chosen.

2. Why Property Insurance Is Extremely Important

Property is usually a high-value, long-term investment. Any unexpected damage can cause massive financial stress.

Without Property Insurance:

- Repair or reconstruction cost must be paid from savings

- Home loan EMI continues even if property is damaged

- Business operations may stop entirely

- Rental income may be lost

With Property Insurance:

- Repair or rebuilding cost is covered

- Financial stability is maintained

- Faster recovery after disasters

- Peace of mind for owners and investors

3. Who Needs Property Insurance?

Property insurance is essential for:

- Homeowners

- Flat & apartment owners

- Landlords

- Commercial property owners

- Shop owners

- Factory & warehouse owners

- Real estate investors

- Businesses with physical assets

If you own a structure or valuable contents, property insurance is necessary.

4. Types of Property Insurance

4.1 Home Insurance Residential Property Insurance

Designed for individual homes, flats, villas, and apartments.

Covers:

- Building structure (walls, roof, foundation)

- Permanent fixtures (plumbing, wiring)

- Household contents (TV, fridge, furniture)

- Optional valuables (jewellery, electronics)

4.2 Commercial Property Insurance

For offices, shops, malls, and commercial buildings.

Covers:

- Commercial building structure

- Office interiors and fittings

- Equipment and furniture

- Stock and inventory

- Important documents

4.3 Fire Insurance

A basic but essential form of property insurance.

Covers damage due to:

- Fire

- Lightning

- Explosion or implosion

- Smoke damage

Used by both residential and commercial property owners.

4.4 Industrial Property Insurance

For factories, plants, and warehouses.

Covers:

- Factory buildings

- Machinery and tools

- Raw materials

- Finished goods

- Storage units

Critical for manufacturing and logistics businesses.

4.5 Landlord Property Insurance

For property owners who rent out buildings.

Covers:

- Structural damage

- Loss of rental income (add-on)

- Legal liability (optional)

5. What Does Property Insurance Cover?

Standard Covered Risks

Most property insurance policies cover:

- Fire and explosion

- Earthquake, flood, cyclone, storm

- Theft and burglary

- Riots, strikes, vandalism

- Electrical short circuit

- Impact damage (vehicle or falling object)

Optional Add-On Covers

- Loss of rent or business income

- Temporary accommodation expenses

- Accidental damage

- High-value contents cover

- Terrorism cover (if selected)

6. What Is NOT Covered?

Property insurance does not cover:

- Normal wear and tear

- Poor construction quality

- Negligence or lack of maintenance

- Intentional damage

- War, nuclear risks

- Gradual deterioration

- Land value

Understanding exclusions is crucial before buying a policy.

7. How Property Insurance Works Step-by-Step Process

- Property owner selects a policy

- Sum insured is decided (reconstruction value)

- Premium is paid (annual or multi-year)

- Damage occurs due to a covered risk

- Claim is reported to insurer

- Surveyor inspects damage

- Loss is assessed

- Claim is approved

- Compensation is paid or repairs arranged

8. How Is the Sum Insured Calculated?

The sum insured is NOT the market value.

It is calculated based on:

- Reconstruction cost

- Carpet/built-up area

- Construction type

- Cost of materials and labour

Land value is never included.

9. Factors Affecting Property Insurance Premium

Premium amount depends on:

- Location of the property

- Age of the building

- Construction type

- Usage (residential/commercial)

- Sum insured

- Add-on covers

- Claim history

High-risk zones attract higher premiums.

10. Claim Settlement Process

To file a claim:

- Inform insurer immediately

- Submit claim form

- Provide photos/videos of damage

- FIR in case of theft or vandalism

- Surveyor inspection

- Repair estimate submission

- Claim approval and payout

Timely reporting improves approval chances.

11. Property Insurance vs Home Loan Insurance

Property Insurance - Home Loan Insurance

Covers physical property

- Covers loan liability

Protects owner

- Protects lender

Covers damage & loss

- Covers borrower’s death

Asset protection

- Loan protection

Both are different and serve separate purposes.

12. Benefits of Property Insurance

- Protects lifetime property investment

- Covers major repair expenses

- Reduces financial risk

- Improves loan eligibility

- Ensures business continuity

- Provides peace of mind

13. Legal & Financial Importance

- Often required by banks for home loans

- Helps meet financial planning goals

- Protects against unforeseen disasters

- Safeguards family and business stability

Conclusion

Property insurance is not an expense—it is financial protection. It shields your home, business, and investment from unpredictable risks, ensuring stability, recovery, and peace of mind. Whether you are a homeowner, landlord, or investor, property insurance is a must-have safeguard in today’s uncertain world.

Frequently Asked Questions

1. Is property insurance mandatory in India?

Not legally mandatory, but compulsory for most home loans.

2. Does property insurance cover land?

No, only structure and contents are covered.

3. Can tenants buy property insurance?

Tenants can insure contents, not the structure.

4. Does property insurance cover floods and earthquakes?

Yes, either included or available as add-ons.

5. How long is property insurance valid?

Usually one year, renewable annually.

6. Can old buildings be insured?

Yes, but premiums may be higher.

7. Is theft covered under property insurance?

Yes, if theft or burglary cover is included.

8. How much compensation will I get?

Based on damage assessed, depreciation, and policy terms.

9. Can I insure a rented-out property?

Yes, through landlord insurance.

10. Is property insurance worth it?

Absolutely—it protects your most valuable asset.