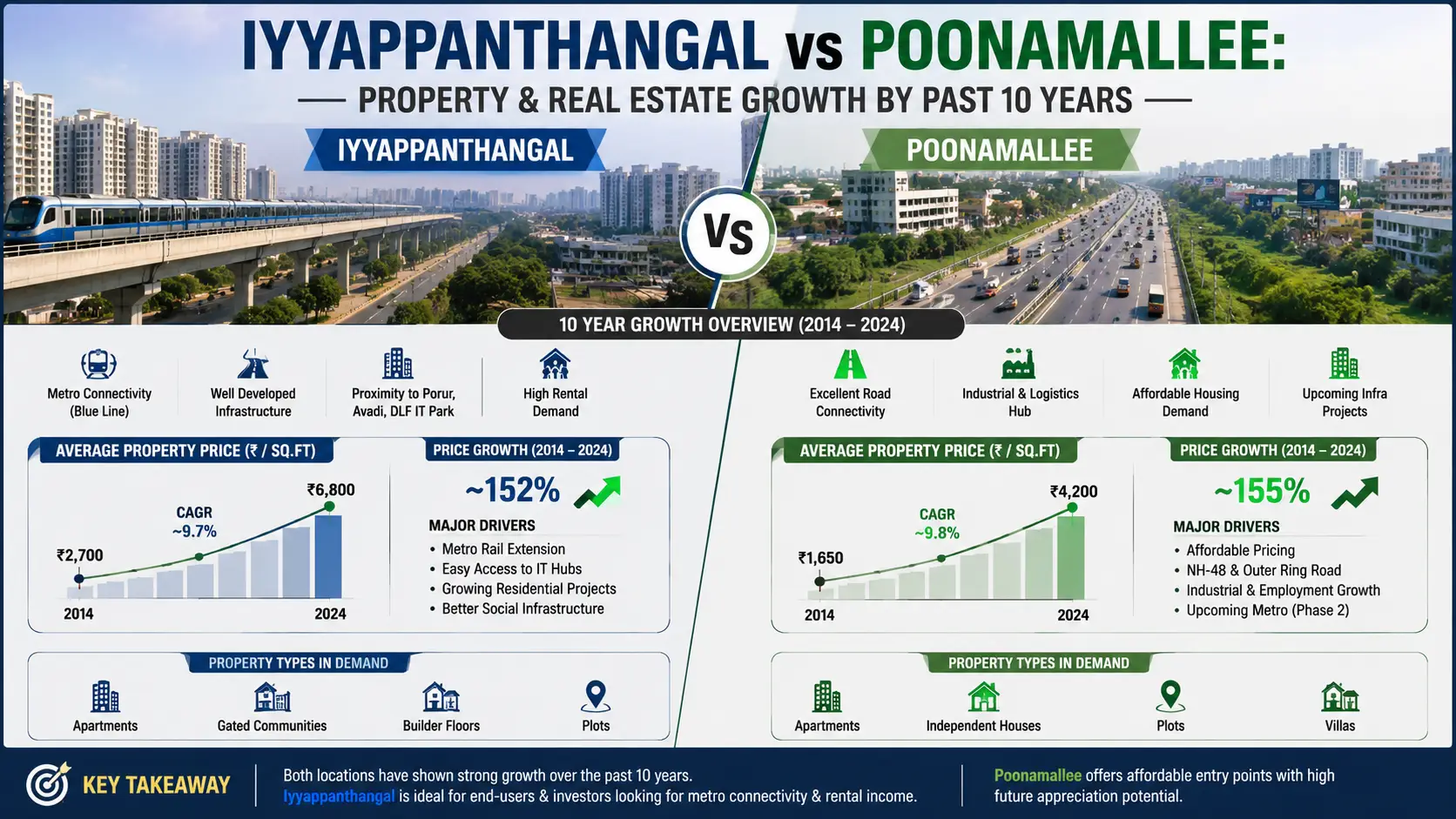

Chennai’s real estate growth has traditionally been driven by the southern and western corridors. However, over the last two decades, the Northern Corridor stretching from Red Hills to Avadi has quietly transformed into a significant affordable and mid-segment residential market. This belt reflects Chennai’s gradual but steady urban expansion driven by infrastructure, employment clusters, and housing demand from end users.

1. Past: Origins and Early Residential Development

Red Hills – From Peripheral Village to Urban Fringe

Red Hills was historically known for its proximity to Puzhal Lake, industrial sheds, transport yards, and agricultural land. Residential development before 2010 was minimal and largely limited to:

- Independent houses

- Worker housing for nearby industrial zones

- Informal plotted layouts

Property values remained low due to limited civic infrastructure, lack of organised developers, and the perception of distance from Chennai’s core.

Avadi – Defence-Led Township

Avadi developed primarily as a defence and manufacturing township, housing establishments such as the Heavy Vehicles Factory (HVF). Residential demand earlier was driven by:

- Defence employees

- Government staffa

- Industrial workers

Housing consisted mainly of plotted homes, government quarters, and low-rise apartments. Until the mid-2000s, Avadi was seen as a self-contained town rather than part of Chennai’s real estate narrative.

2. Transition Phase: 2010–2020 – The Growth Foundation

Between 2010 and 2020, the Red Hills–Avadi corridor began witnessing structural transformation.

Key Drivers During This Period

- Expansion of the Outer Ring Road

- Improved road connectivity to Ambattur, Madhavaram, and Thiruvallur

- Saturation and price escalation in central Chennai

- Rising demand for affordable housing from first-time buyers

Land parcels along this belt attracted small and mid-sized developers. Plotted developments, budget apartments, and row houses became common. Prices started appreciating steadily but remained within affordable limits compared to southern corridors.

3. Present Market Scenario (2025–2026)

Residential Profile Today

The Northern Corridor is now defined by:

- Affordable and mid-segment apartments

- Gated villa communities in pockets

- Approved residential plots

- Rental housing for industrial and logistics workforce

Red Hills – Emerging Residential Zone

Red Hills has evolved into a budget-driven residential micro-market. Demand is largely end-user oriented, supported by:

- Proximity to logistics parks and industrial clusters

- Gradual improvement in social infrastructure

- Lower entry price compared to established suburbs

Residential supply is dominated by:

- Low-rise apartments

- Independent houses

- DTCP and CMDA-approved plots

Avadi – Stable and Mature Suburb

Avadi today functions as a well-established residential suburb within Chennai’s expanded urban limits. Key characteristics include:

- Strong suburban rail connectivity

- Presence of schools, hospitals, and markets

- Consistent rental demand

Apartments in Avadi command higher value than Red Hills due to better civic maturity and long-standing residential character.

4. Price Movement: Past vs Present

Period / Red Hills (Rs /sq.ft) / Avadi (Rs/sq.ft)

2012–2014

- 1,500 – 2,000

- 2,800 – 3,500

2018–2020

- 3,000 – 4,000

- 4,500 – 5,500

2025–2026

- 4,500 – 6,500

- 6,000 – 8,000

Price growth has been gradual and organic, driven more by end-user demand than speculative investment — a key strength of this corridor.

5. Infrastructure Impact on Residential Demand

The corridor benefits from:

- Road connectivity linking northern and western Chennai

- Suburban railway access from Avadi

- Proximity to industrial employment zones

- Gradual expansion of civic amenities

Unlike speculative corridors, development here follows population and employment movement, making the market more resilient.

6. Future Outlook: 2026–2035

The future of the Red Hills–Avadi residential belt is shaped by planned infrastructure, urban spillover, and affordability demand.

Expected Trends

- Continued demand for affordable housing

- Increase in gated community developments

- Gradual land value appreciation

- Higher rental absorption due to industrial growth

Projected annual appreciation is expected to remain moderate and stable, rather than aggressive — appealing to long-term homeowners and conservative investors.

7. Investment vs End-Use Perspective

- End Users: Strong suitability due to affordability, improving infrastructure, and livability

- Long-Term Investors: Stable capital appreciation with low volatility

- Rental Market: Consistent but moderate yields driven by workforce housing demand

This corridor is less speculative and more utility-driven, which supports sustained residential growth.

8. Conclusion: Northern Corridor’s Real Estate Identity

The Red Hills to Avadi corridor represents Chennai’s next phase of inclusive urban growth. It is not a high-luxury or speculative market, but a fundamentally strong residential zone driven by real housing needs. As Chennai continues to expand beyond traditional hotspots, this northern belt is positioned as a practical, affordable, and stable residential corridor — evolving steadily rather than explosively.

Live Services

Live Services