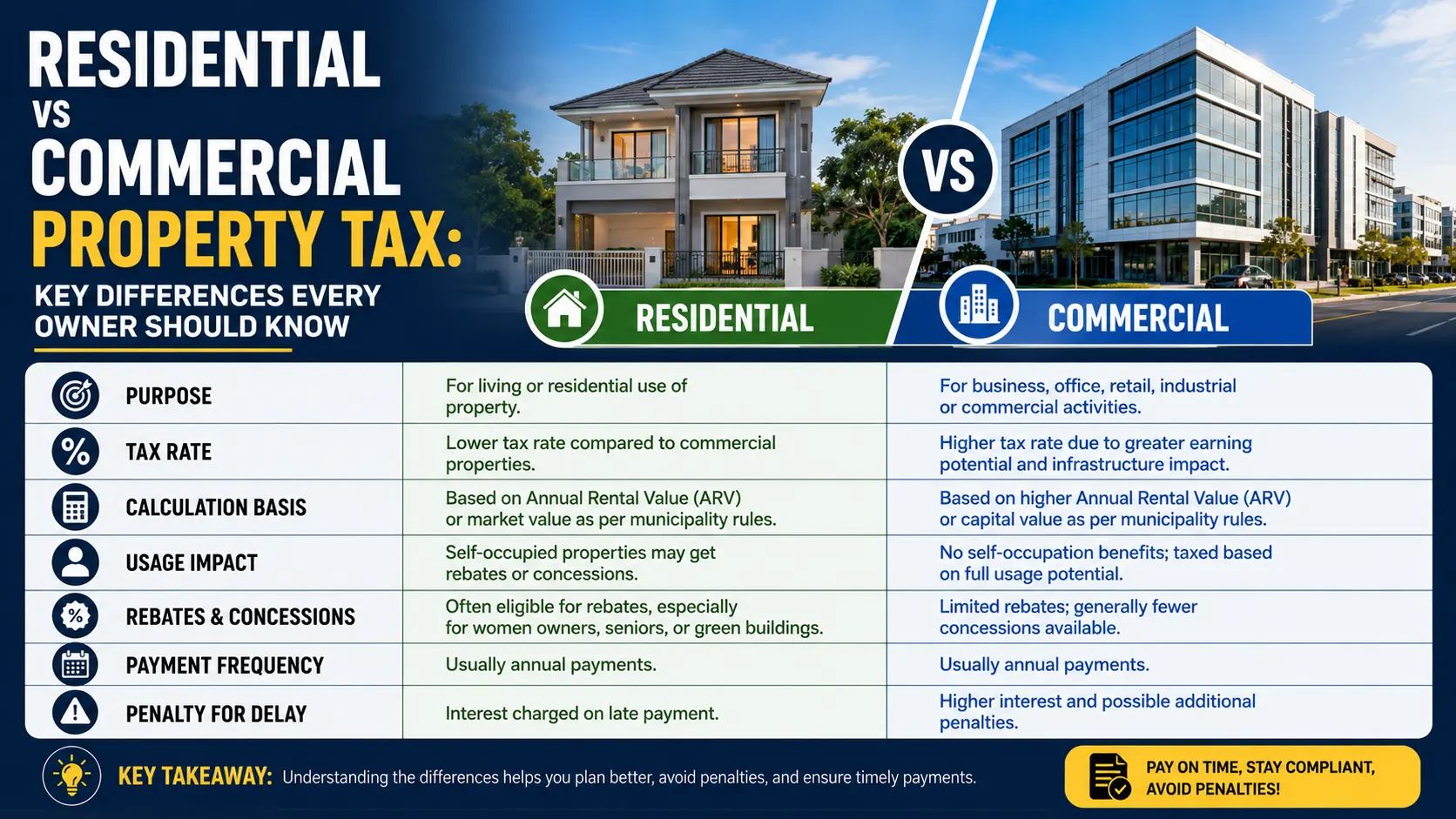

Property tax is a mandatory local tax levied by municipal authorities on property owners for funding civic infrastructure such as roads, drainage, water supply, waste management, street lighting, and public services. The tax system clearly differentiates residential and commercial properties because their purpose, economic value, and impact on civic infrastructure are fundamentally different.

1. Why Property Tax Is Classified by Usage

Municipal taxation follows a usage-based principle, not ownership-based.

- Residential properties are meant for human habitation

- Commercial properties are meant for economic activity and income generation

Since commercial properties:

- Generate revenue

- Increase foot traffic

- Use more civic resources

They are taxed at higher rates.

2. What Is a Residential Property For Tax Purposes

A residential property is one that is used exclusively for living purposes.

Includes:

- Individual houses

- Apartments and flats

- Residential portions of mixed-use buildings

- Rented homes used only for residence

Important Clarification:

- Ownership does not matter

- Rental status does not matter

- Only usage matters

If people live there, it is residential—even if the owner earns rent.

3. What Is a Commercial Property For Tax Purposes

A commercial property is one used partly or fully for business, professional, or income-generating activities.

Includes:

- Shops and retail outlets

- Offices and corporate buildings

- IT parks and business centers

- Warehouses and godowns

- Hotels, restaurants, hospitals

- Private schools, colleges, coaching centers

- Clinics, salons, gyms

Even non-profit activities may still be classified as commercial if they operate regularly.

4. How Municipal Authorities Determine Property Type

Classification is based on:

- Physical inspection

- Declared usage in records

- Utility usage patterns

- Signboards or advertisements

- Business registrations linked to address

- Complaints or surveys

Zoning approval alone does not override actual usage.

5. Residential Property Tax – End-to-End

5.1 Tax Objective

- Keep housing affordable

- Encourage ownership

- Provide basic civic services

5.2 Key Factors Used in Calculation

- Built-up or plinth area

- Location and ward

- Type of construction

- Age of building (depreciation)

- Occupancy (self-occupied or rented)

5.3 Rate Characteristics

- Lower tax rates

- Often slab-based

- Gradual increases over time

- 5.4 Rebates & Concessions

Common for:

- Senior citizens

- Disabled owners

- Self-occupied homes

- Early or lump-sum payment

5.5 Enforcement Level

- Moderate

- Focused mainly on payment delays

- Misuse action is less frequent unless reported

6. Commercial Property Tax – End-to-End

6.1 Tax Objective

- Capture revenue from income-generating assets

- Offset higher infrastructure load

6.2 Key Factors Used in Calculation

- Built-up area

- Nature of business

- Location and commercial importance

- Rental or capital value

- Intensity of usage (footfall, hours)

6.3 Rate Characteristics

- 2 to 3 times residential rates (or more)

- No social welfare consideration

- Faster escalation over time

6.4 Rebates & Concessions

- Rare or nonexistent

- Vacancy usually does not reduce tax

- Loss-making business still taxed

6.5 Enforcement Level

- High scrutiny

- Inspections and audits common

- Strong penalties for violations

7. Mixed-Use Properties

Properties used partly residential and partly commercial are taxed separately.

Example:

- Ground floor shop → Commercial tax

- Upper floor residence → Residential tax

Authorities measure and assess each portion independently.

8. Renting and Its Tax Impact

Residential Rental

- Renting for living purposes does not change classification

- Tax remains residential

Commercial Rental

- Leasing to any business = commercial tax

- Owner’s personal income status is irrelevant

9. Reclassification & Misuse

What Triggers Reclassification

- Running offices from homes

- Clinics or tuition centers in houses

- Shops in residential units

Consequences

- Retrospective commercial tax

- Penalty and interest

- Possible sealing or legal notice

Reclassification can apply from the date misuse started, not inspection date.

10. Payment Cycle & Compliance

Residential

- Annual or half-yearly payments

- Grace periods common

Commercial

- Strict payment deadlines

- Higher late fees

- Legal recovery proceedings more likely

11. Legal & Financial Impact Over Time

Residential Property

- Predictable tax burden

- Slow escalation

- Limited financial stress

Commercial Property

- Rising operational cost

- Direct impact on profitability

- Tax planning becomes necessary

Over long holding periods, commercial tax significantly affects net returns.

12. Why Commercial Property Is Taxed More

Municipal reasoning:

- Businesses earn income from property

- Higher wear and tear on infrastructure

- Increased demand for civic services

- Ability to absorb higher tax

Residential property is protected as a social necessity, not a revenue engine.

Conclusion

Residential and commercial property taxes differ not just in rate, but in philosophy, enforcement, and long-term financial impact. Residential tax protects housing affordability, while commercial tax extracts value from income-producing real estate. Understanding this distinction is critical because usage—not ownership—defines liability, and mistakes can lead to heavy retrospective costs.

Frequently Asked Questions

Q1. Does renting a house make it commercial?

No. Renting for residential living keeps it residential.

Q2. What if I work from home?

Casual remote work is usually ignored. Registered offices, signage, or customer visits may trigger reclassification.

Q3. Can authorities charge past commercial tax?

Yes. Retrospective assessment is legally permitted.

Q4. Is vacant commercial property taxed less?

No. Vacancy does not change classification.

Q5. Can a property be both residential and commercial?

Yes. Mixed-use properties are taxed proportionately.

Q6. Who decides classification?

The local municipal authority based on inspection and records.

Q7. Can classification be appealed?

Yes, but proof of actual usage is mandatory.

Q8. Does higher tax affect resale?

Indirectly yes, due to higher ownership costs.

Q9. Is property tax different from income tax?

Yes. Property tax is a municipal levy; income tax is a central tax.