Role of the Reserve Bank of India (RBI)

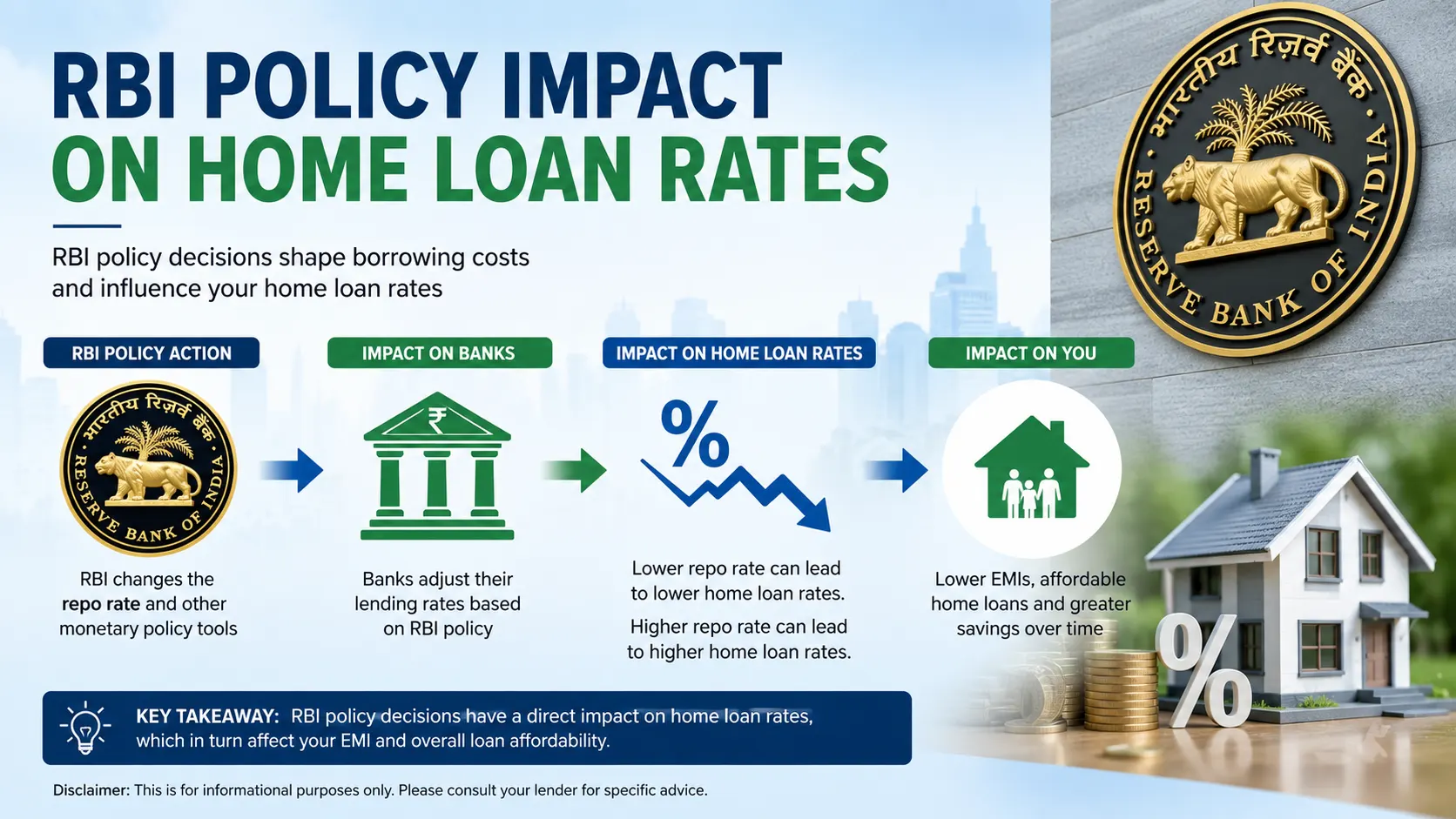

The Reserve Bank of India is the central banking authority of the country. Its primary responsibilities include controlling inflation, ensuring financial stability, regulating banks, and managing monetary policy. RBI’s monetary policy decisions directly influence interest rates in the economy, including home loan interest rates offered by banks and housing finance companies. RBI does not decide home loan rates directly. Instead, it controls policy interest rates, which determine the cost at which banks borrow money. Banks use this cost as the base for fixing lending rates for customers.

Monetary Policy and the Monetary Policy Committee

RBI’s monetary policy decisions are taken by the Monetary Policy Committee (MPC).

The MPC consists of six members and meets regularly to assess economic conditions such as inflation, growth, liquidity, and global trends.

Based on this assessment, the MPC may:

- Reduce policy rates

- Increase policy rates

- Keep policy rates unchanged

These decisions directly influence interest rates across the banking system.

Key RBI Policy Rates That Affect Home Loan Interest Rates

1. Repo Rate

The repo rate is the most important policy rate. It is the rate at which RBI lends short-term funds to commercial banks.

- When the repo rate is reduced, banks can borrow money at a lower cost.

- When the repo rate is increased, borrowing from RBI becomes more expensive.

Since banks use borrowed funds to lend to customers, changes in the repo rate influence the interest rates charged on home loans.

2. Reverse Repo Rate

The reverse repo rate is the rate at which banks deposit excess funds with RBI.

- A higher reverse repo rate encourages banks to park money with RBI rather than lend.

- A lower reverse repo rate encourages banks to lend more.

This indirectly affects the availability and pricing of home loans.

3. External Benchmark Lending Rate System

Under RBI guidelines, most floating-rate home loans are linked to an external benchmark, usually the repo rate.

Key features:

- Interest rate changes are automatically linked to RBI’s repo rate movements

- Reset happens at predefined intervals (monthly or quarterly)

- Improves transparency and faster transmission of policy changes

Because of this system, RBI policy changes now reach home loan borrowers more efficiently than earlier.

4. MCLR and Base Rate System (Older Loans)

Loans sanctioned earlier may be linked to:

- MCLR (Marginal Cost of Funds Based Lending Rate)

- Base Rate

Under these systems:

- RBI policy changes affect banks’ internal funding costs

- Rate transmission is slower

- Banks may delay or partially pass on rate changes

How RBI Policy Decisions Affect Home Loan Rates

RBI Rate Cut Scenario

When RBI reduces the repo rate:

- Banks’ cost of borrowing decreases

- Lending rates, including home loan rates, generally decline

- Floating-rate home loan interest rates are revised downward

- Monthly EMIs reduce or loan tenure shortens

- Overall interest burden on borrowers decreases

RBI Rate Hike Scenario

When RBI increases the repo rate:

- Banks face higher borrowing costs

- Home loan interest rates rise for floating-rate borrowers

- EMIs increase or loan tenure extends

- Total interest paid over the loan period increases

RBI Rate Pause Scenario

When RBI keeps rates unchanged:

- Home loan interest rates remain stable

- EMIs do not change

- Borrowers experience predictability in repayments

Fixed-Rate and Floating-Rate Home Loans

Floating-Rate Home Loans

- Directly impacted by RBI policy changes

- Interest rates change based on benchmark revisions

- EMIs fluctuate over the loan tenure

Fixed-Rate Home Loans

- Interest rate remains constant for a fixed period

- RBI policy changes do not affect rates during this period

- Impact is seen only after the fixed-rate period ends

RBI Policy Impact Over the Long Term

Home loans usually have long tenures ranging from 15 to 30 years. During this period:

- Multiple RBI policy cycles occur

- Interest rates move up and down

- Cumulative impact of RBI decisions significantly affects total interest paid

Thus, RBI policy plays a crucial role in determining the long-term cost of housing finance.

Broader Economic Link

RBI policy impacts not only home loan rates but also:

- Housing affordability

- Demand for residential property

- Construction and allied industries

- Overall economic growth

Lower interest rates generally stimulate housing demand, while higher rates can slow borrowing and housing activity.

Frequently Asked Questions

1. Does RBI directly set home loan interest rates?

No. RBI sets policy rates. Banks decide home loan rates based on these policy rates and their internal costs.

2. Why do floating-rate home loans change more frequently?

Because they are linked to external benchmarks such as the repo rate, which changes based on RBI policy decisions.

3. Are existing borrowers affected by RBI policy changes?

Yes. Existing borrowers with floating-rate loans experience changes in EMIs or tenure after RBI rate changes.

4. Why is the impact slower for some home loans?

Loans linked to MCLR or base rate depend on banks’ internal cost calculations, leading to delayed transmission.

5. Does RBI policy affect total interest paid on a home loan?

Yes. Even small changes in interest rates, when applied over long tenures, significantly affect total interest outgo.

6. Can RBI policy influence housing demand?

Yes. Lower interest rates make home loans cheaper, increasing demand, while higher rates reduce affordability.

7. Is RBI policy relevant throughout the loan tenure?

Yes. RBI policy remains relevant for the entire duration of a floating-rate home loan.

8. Do fixed-rate loans completely escape RBI policy impact?

Only during the fixed-rate period. After the reset, RBI policy indirectly affects the new rate.