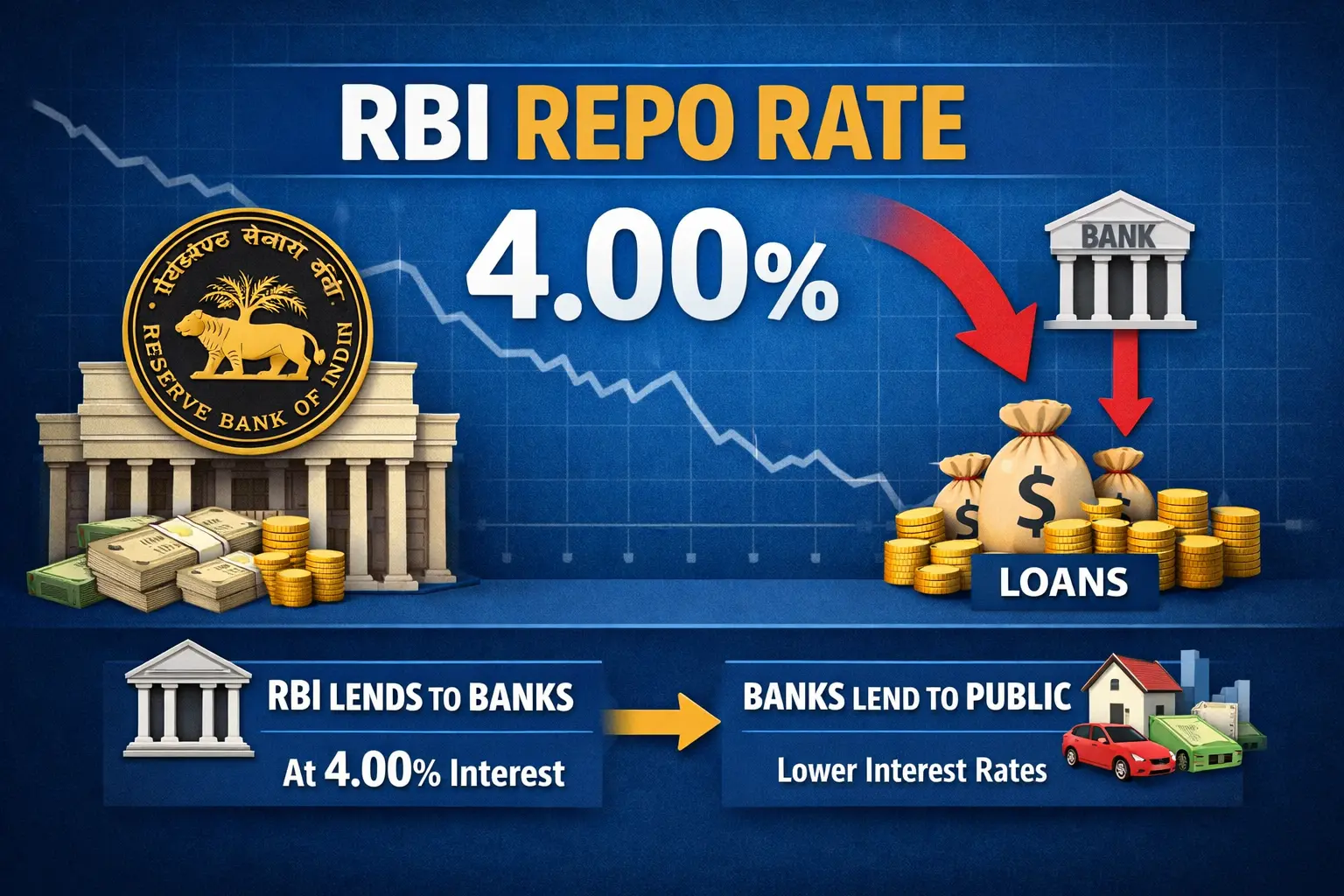

The Monetary Policy Committee of the central bank, in its meeting held on April 8, decided to keep the repo rate unchanged at 5.25 per cent, extending the pause after a series of interest rate reductions over the past year. For home loan borrowers, this decision brings much-needed stability at a time when interest rate movements have been closely watched. As most home loans in India are linked to external benchmarks such as the repo rate, an unchanged policy rate means that equated monthly installments (EMIs) are likely to remain steady in the near term. Banks are also expected to maintain their current lending rates unless there is a significant change in liquidity conditions or a shift in the overall monetary policy stance. This stability allows both existing and prospective borrowers to plan their finances with greater certainty, without the immediate concern of rising EMIs. While the latest decision does not provide fresh relief in the form of further rate cuts, borrowers have already benefited substantially from the cumulative reduction of 125 basis points in the repo rate since early 2025. These reductions have translated into lower borrowing costs, meaningful EMI relief, and significant interest savings over the full tenure of home loans—particularly for borrowers whose loans have fully adjusted to the lower rate cycle. For instance, on a home loan of Rs 50 lakh with a tenure of 20 years, the reduction in interest rates has resulted in an EMI saving of roughly Rs 3,050 per month, along with a total interest saving of about Rs7.34 lakh over the life of the loan. In the case of a Rs 75 lakh loan, the monthly EMI savings are approximately Rs 5,800, while the overall interest savings amount to nearly Rs 13.94 lakh. By holding rates steady, the current policy decision ensures that these gains remain intact, offering continued relief and predictability for home loan borrowers.

RBI Repo Rate at 5 percentage How a Rs 75 Lakh Home Loan Can Save Up to Rs 14 Lakh

Apr 09 2026

Latest Newsletter

Chennai Real Estate Developers Request Clear Guidelines on Metro Corridor FSI

Jul 25 2026

Centre Reorganizes Ministry of Housing and Urban Affairs

Jul 24 2026

Ramsar Protection Freeze Delays Construction Across South Chennai

Jul 23 2026

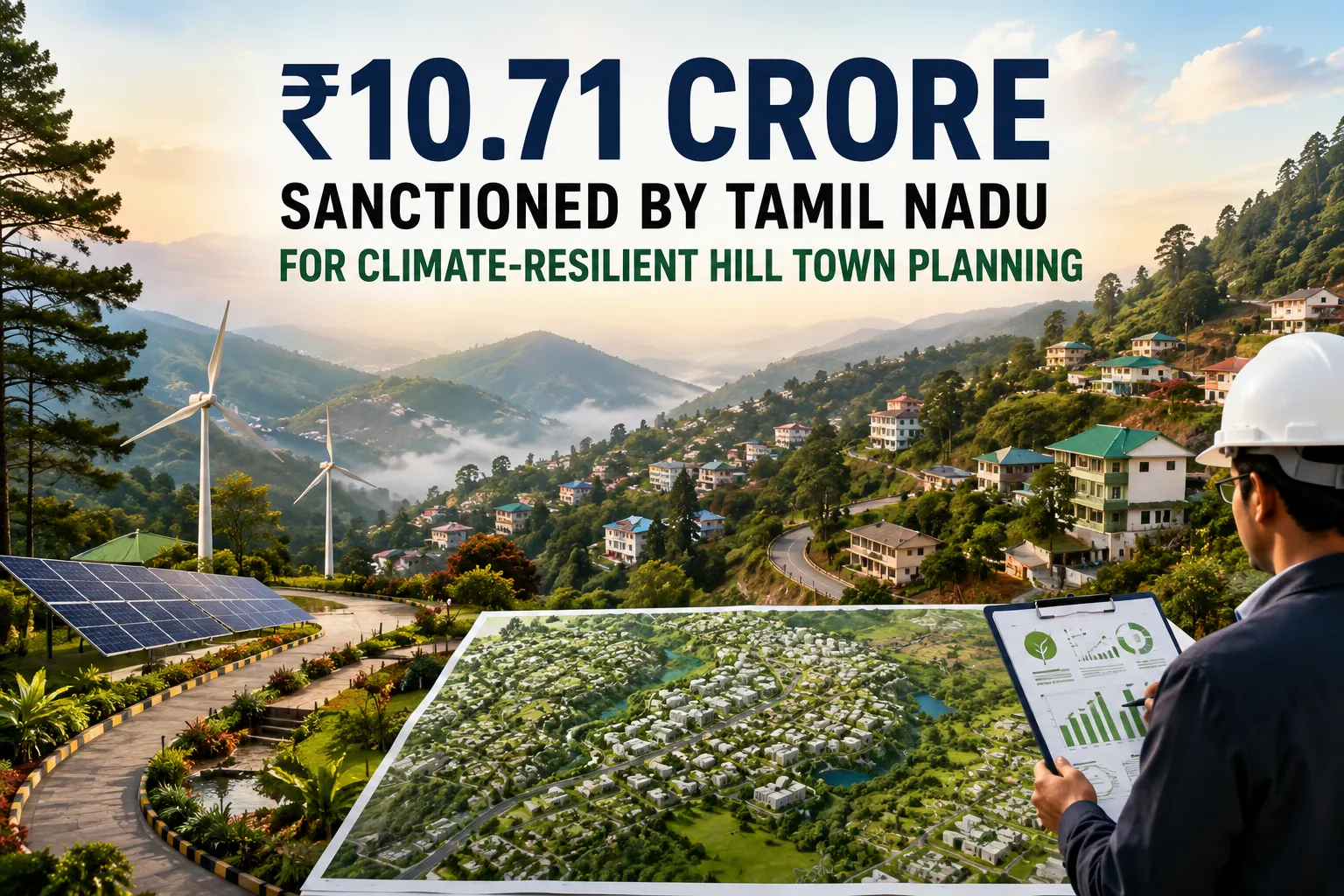

Tamil Nadu Approves Rs 10.71 Crore for Climate Resilient Hill Town Master Plans

Jul 22 2026

Chennai Corporation Collects Rs 103 Crore in Property Tax Within 14 Days

Jul 21 2026