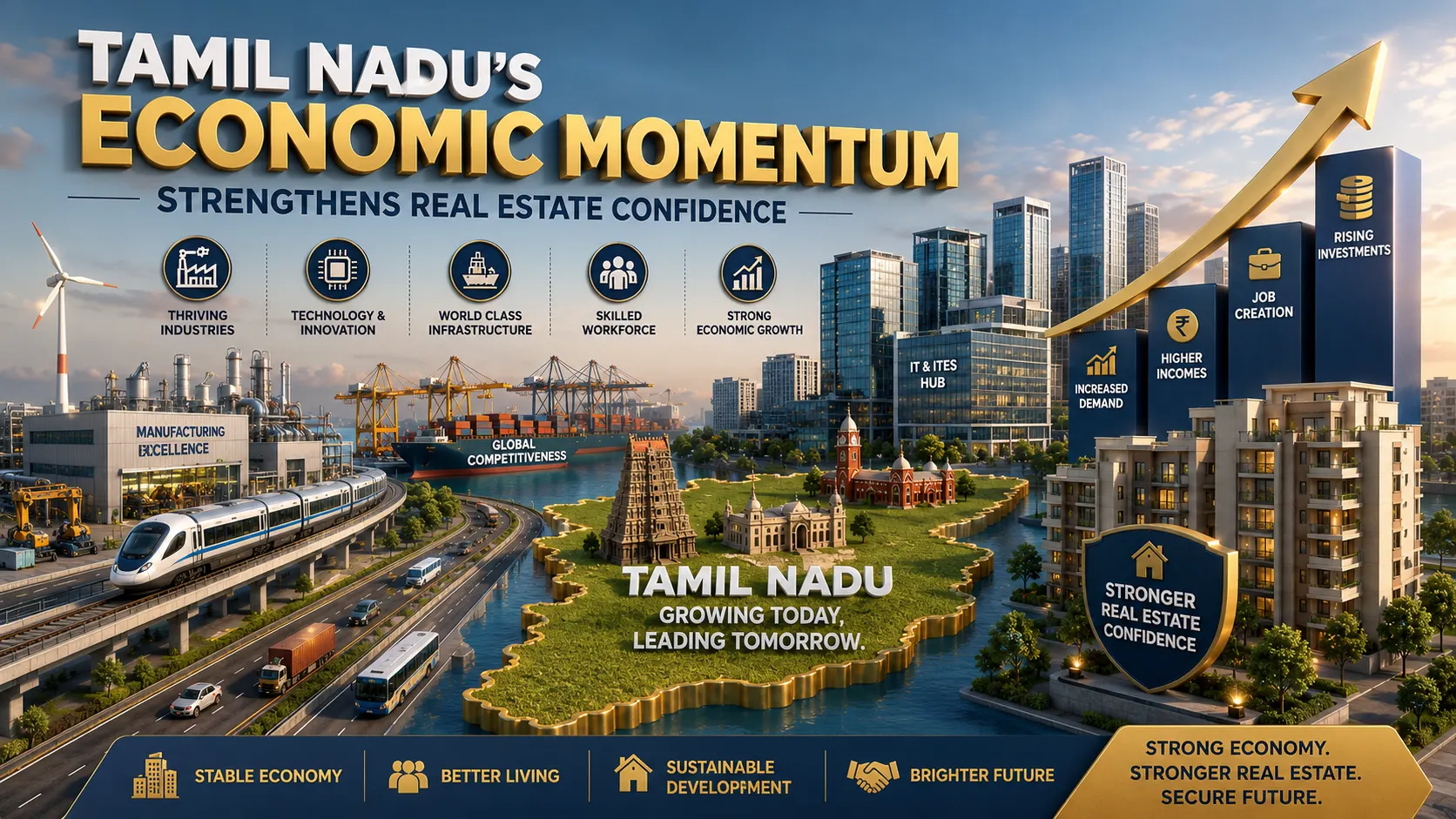

Surpassing the long-standing dominance of the IT sector, Global Capability Centres (GCCs) have emerged as the primary growth engine of Chennai’s commercial real estate market in 2025. GCCs accounted for 51% of the city’s total gross office space leasing, overtaking all other sectors and compensating for a visible slowdown in demand from traditional IT and IT-enabled services. Out of the 8.4 million sq ft of gross office leasing recorded during the year, GCCs alone absorbed 4.3 million sq ft, underlining their growing strategic importance in the city’s office ecosystem. This performance placed Chennai well ahead of the national trend, where GCCs contributed 41% of total office absorption across India, an increase from 36% in the previous year. Office space absorption continues to act as a reliable indicator of sectoral expansion, with data pointing to a sustained upward trajectory. GCC-related leasing witnessed consistent growth, rising from 2.0 million sq ft (27% share) of the 7.4 million sq ft leased in 2023, to 3.29 million sq ft (41% share) of the 8.1 million sq ft leased in 2024, before crossing the halfway mark in 2025. The Chennai office market experienced a notable sectoral realignment during 2025, reflecting broader economic shifts and evolving industry dynamics. As GCC activity accelerated, supply conditions tightened. New office completions stood at 3.9 million sq ft, while net office absorption reached 5.6 million sq ft, indicating demand significantly outpaced supply. This translated into a 12% year-on-year growth in absorption, exceeding the 10% average growth recorded across India’s top seven office markets. Chennai also stood out as the only major metropolitan market with single-digit vacancy levels, with vacancy rates declining from 9.2% to 8.8% during the year. The tightening market conditions contributed to upward pressure on rents, with average monthly office rentals rising by 5% year-on-year to nearly ?79 per sq ft. Looking ahead, market indicators suggest that Chennai’s office sector is poised to maintain positive momentum through 2026, supported by sustained demand from GCCs. Beyond the metropolitan region, Coimbatore has emerged as a leading Tier-II city for GCC expansion, benefiting from improved infrastructure, talent availability, and cost advantages. While Chennai and Mumbai continue to function as key data centre hubs in the country, Coimbatore and Madurai are increasingly gaining traction as emerging data centre destinations, further strengthening Tamil Nadu’s position as a diversified commercial and digital infrastructure hub.

https://www.livehomes.in/news_letter