The interest rate on a home loan plays a crucial role in determining both your monthly Equated Monthly Installment (EMI) and the total cost of the loan over its entire tenure. Even a small difference in the interest rate can lead to substantial savings or additional costs when spread across several years. Therefore, securing the lowest possible home loan interest rate is essential for long-term financial planning. When taking a home loan, borrowers can choose a repayment tenure based on their financial comfort, allowing them to repay the loan through manageable monthly installments. However, the interest rate offered on a home loan is not fixed for everyone and depends on several important factors. One of the most significant factors is the credit score of the borrower. A higher credit score reflects strong credit discipline and lower risk for lenders, which often results in access to lower interest rates and better loan terms. Borrowers with good credit scores typically benefit from reduced EMIs and lower overall interest outgo, while those with lower scores may be charged higher rates. Another important determinant is the loan-to-value (LTV) ratio, which represents the proportion of the property value financed through the loan. A lower LTV ratio generally indicates lower risk for the lender and can help borrowers secure more favorable interest rates. Similarly, income stability and repayment capacity play a vital role, as lenders assess whether the borrower can comfortably meet repayment obligations over the chosen tenure. The loan tenure itself also affects the interest rate and EMI structure. While longer tenures reduce monthly EMI amounts, they increase the total interest paid over time. Additionally, broader economic factors such as the policy interest rate set by monetary authorities influence lending rates, especially for loans linked to benchmark rates. The comparison table referenced provides an overview of home loan interest rates for loan amounts above Rs 75 lakh, covering both public sector and private sector lenders. This comparison helps borrowers understand how interest rates vary across different institutions and highlights the importance of evaluating multiple options before making a decision. By analyzing such comparisons, borrowers can identify lenders offering more competitive rates and choose a loan that best aligns with their financial goals. In summary, obtaining a home loan at a lower interest rate—supported by a strong credit profile and favorable loan terms—can significantly reduce EMIs and generate meaningful savings over the life of the loan.

Lowest Home Loan Interest Rates in India Banks Offering the Lowest EMI

Mar 25 2026

Latest Newsletter

Does Your Real Estate Project Require Registration Process, Documents, and Benefits Explained

Jun 24 2026

Power Shutdown Scheduled Across Several Chennai Areas on Wednesday

Jun 23 2026

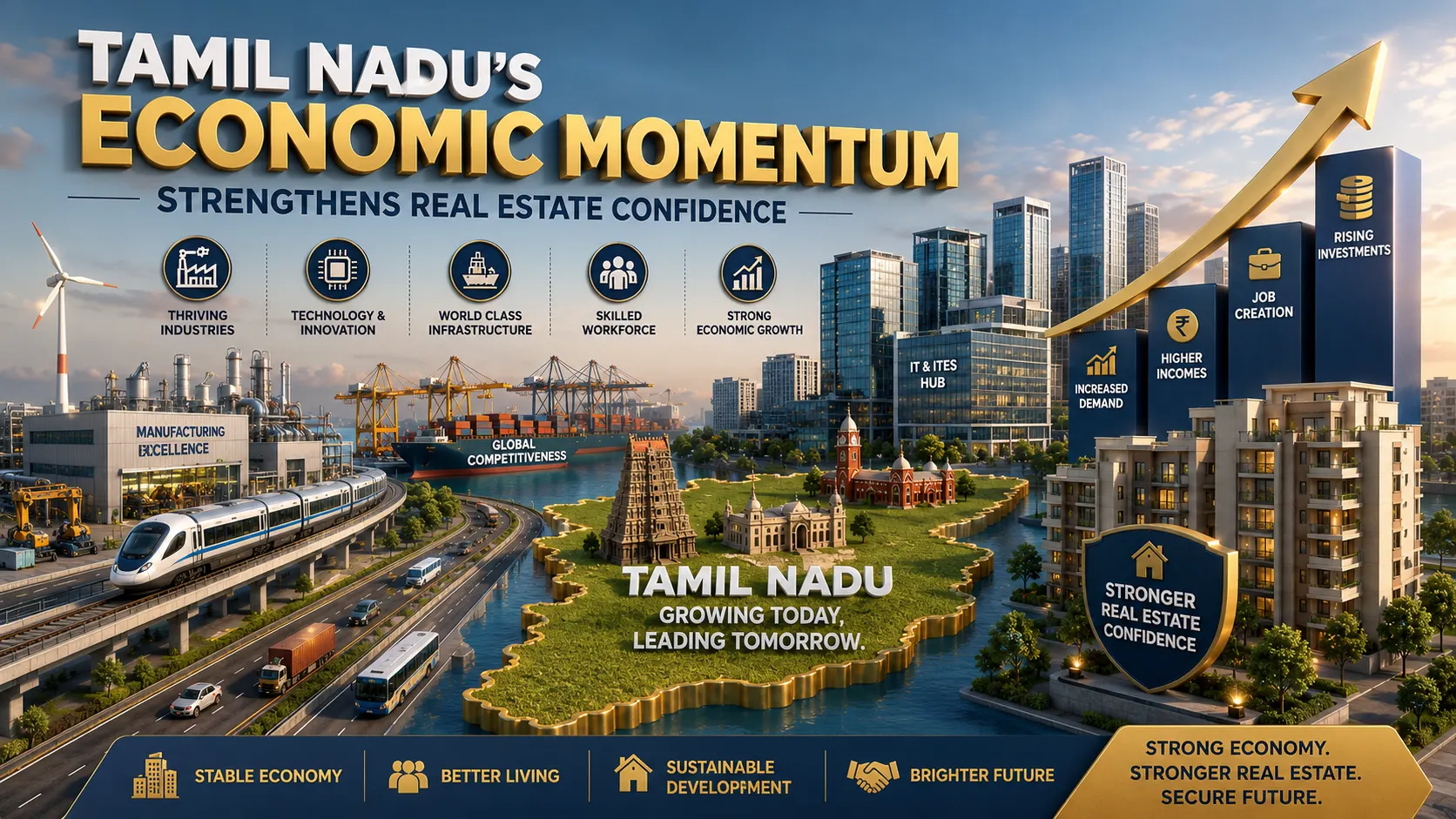

Tamil Nadu’s Economic Momentum Strengthens Real Estate Confidence

Jun 22 2026

Chennai development body to withdraw from construction, prioritise urban planning

Jun 20 2026

Rs 2,000 crore housing project near Pallikaranai Ramsar site stopped by TN govt

Jun 19 2026