Many homeowners unknowingly carry the weight of their home loans far longer than necessary. Instead of treating a mortgage as a strategic financial tool, it is often viewed as a fixed monthly obligation—much like a subscription that must simply be paid for decades. This passive approach can result in borrowers paying lakhs more in interest and remaining in debt well into their peak earning years. A simple but highly effective repayment strategy can significantly reduce both the tenure and total cost of a home loan. By making small, planned adjustments—such as paying one extra EMI each year or gradually increasing EMI amounts—borrowers can shorten a 20-year home loan by several years while saving a substantial amount in interest. One of the most powerful methods is adding just one additional EMI annually. This extra payment is typically applied directly to the principal rather than interest. As a result, the outstanding loan balance reduces faster, which in turn lowers the interest charged in subsequent years. Over time, this single annual payment can reduce a 20-year home loan to approximately 15 years, eliminating dozens of interest-heavy months. Another highly effective approach is incrementally increasing EMI payments by around 5% each year, ideally aligned with annual salary growth. Since income usually rises over time while EMIs remain fixed, redirecting a portion of increased earnings toward loan repayment creates a compounding benefit. With this strategy, a 20-year home loan can potentially be repaid in about 12 years, saving nearly Rs 30 lakh in interest on a Rs 50 lakh loan at an interest rate of 9%. The logic behind these strategies is straightforward. In long-term loans, banks earn a significant portion of their profits from interest accrued over the later years. Borrowers who make only fixed EMIs allow interest to compound for longer periods, unknowingly extending the most expensive phase of the loan. By reducing the principal earlier, borrowers limit the interest base and regain financial control. This approach also changes how mortgage payments are perceived. Instead of being a rigid monthly expense, EMIs become a flexible financial lever. Any extra amount paid toward the principal delivers a guaranteed, risk-free return equivalent to the loan’s interest rate—often higher than many traditional investment options, without exposure to market volatility. Beyond savings, this strategy promotes disciplined financial planning. Committing to small, consistent increases or an extra EMI each year builds a proactive money mindset. It shows that meaningful financial progress doesn’t require drastic sacrifices—just intentional, well-timed decisions. Ultimately, reducing a home loan tenure by even a decade is more than an interest-saving exercise. It accelerates financial freedom, improves cash flow in later years, and transforms a standard repayment schedule into an optimized path toward long-term wealth stability.

How a Minor EMI Change Can Save You Lakhs and Close Your Home Loan Faster

Mar 23 2026

Latest Newsletter

Power Shutdown Scheduled Across Several Chennai Areas on Wednesday

Jun 23 2026

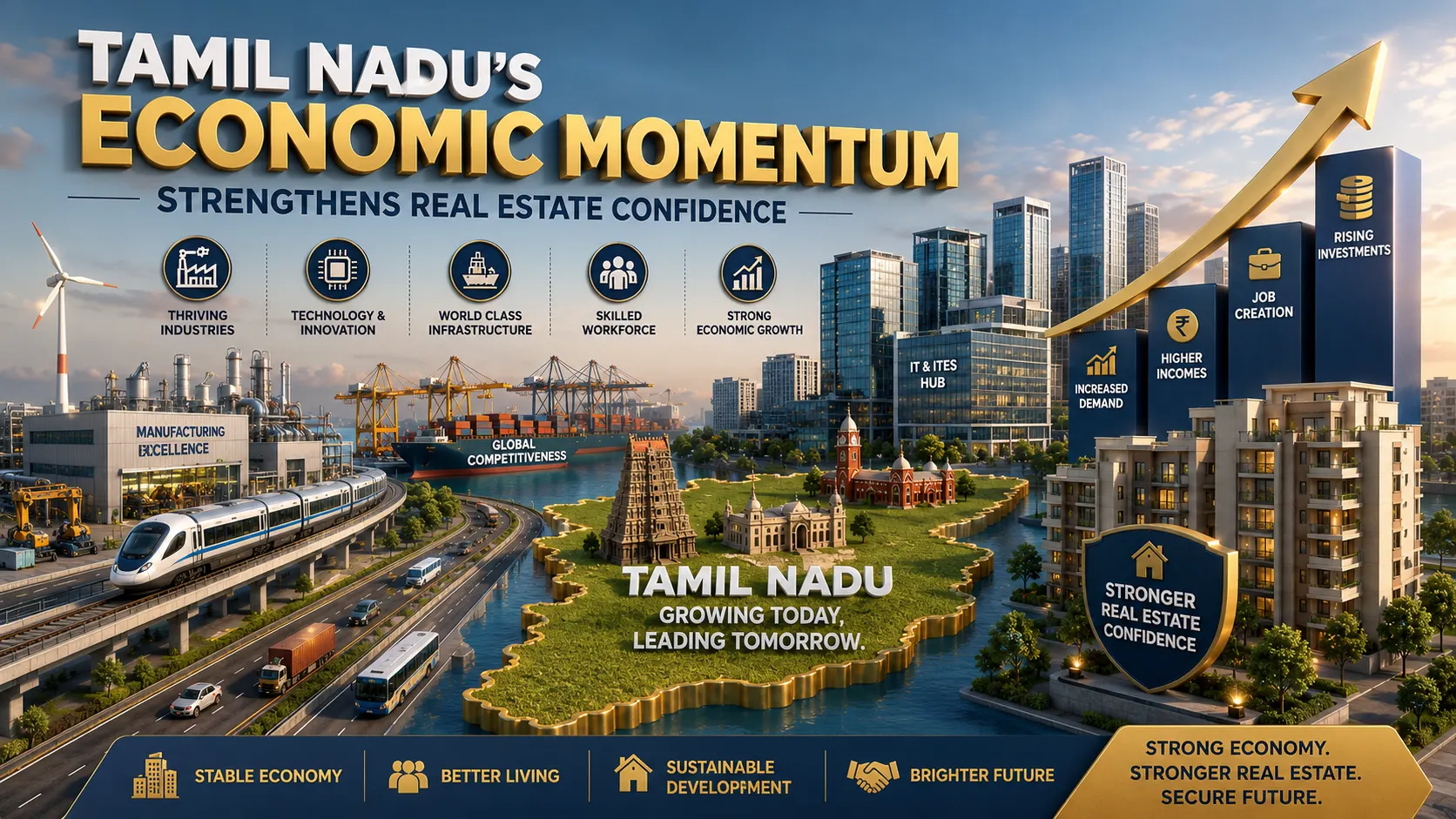

Tamil Nadu’s Economic Momentum Strengthens Real Estate Confidence

Jun 22 2026

Chennai development body to withdraw from construction, prioritise urban planning

Jun 20 2026

Rs 2,000 crore housing project near Pallikaranai Ramsar site stopped by TN govt

Jun 19 2026

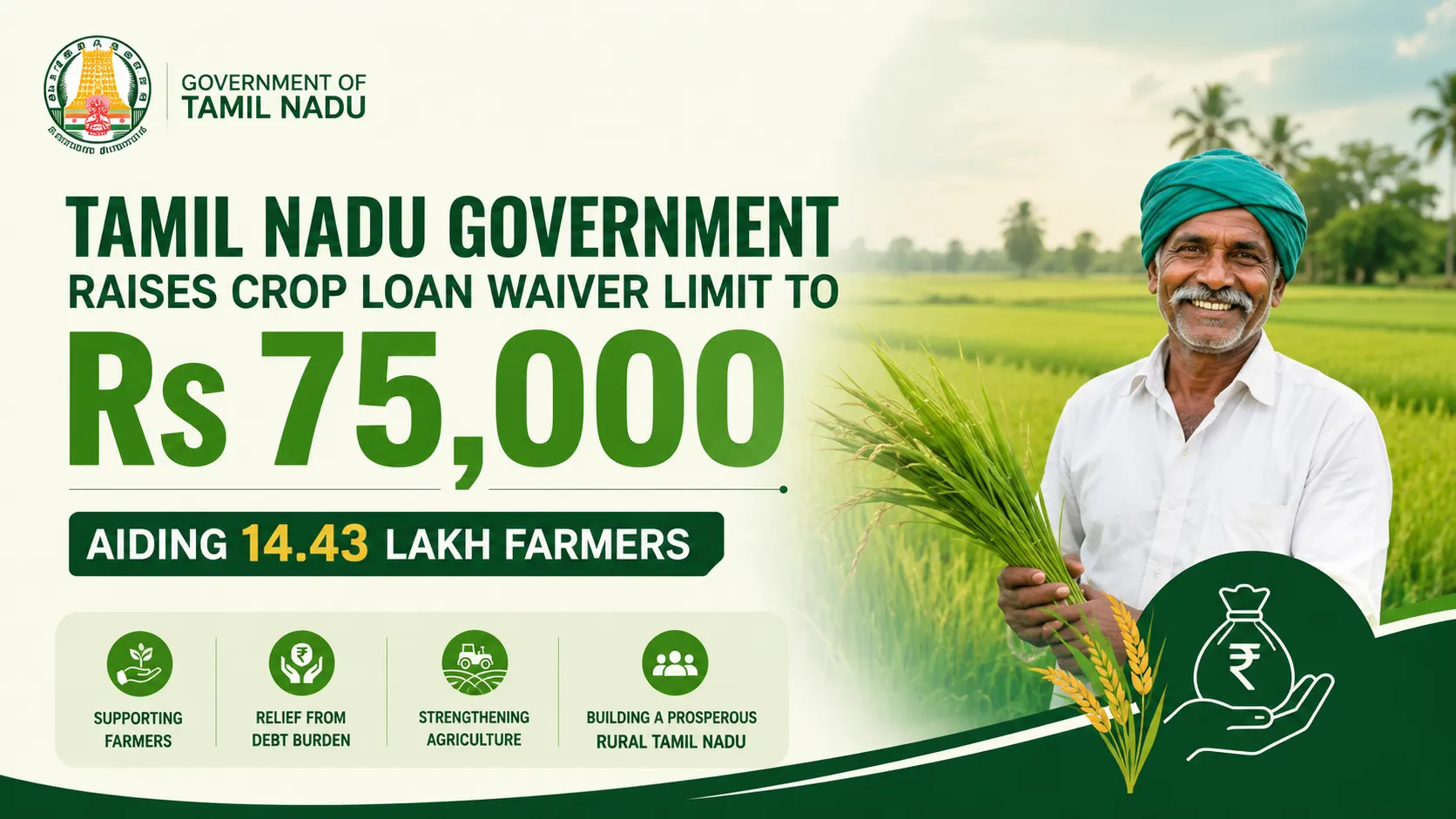

Tamil Nadu Government Raises Crop Loan Waiver Limit to Rs 75,000, Aiding 14.43 Lakh Farmers

Jun 18 2026