Live Services

Live Services

23, Jun 2026

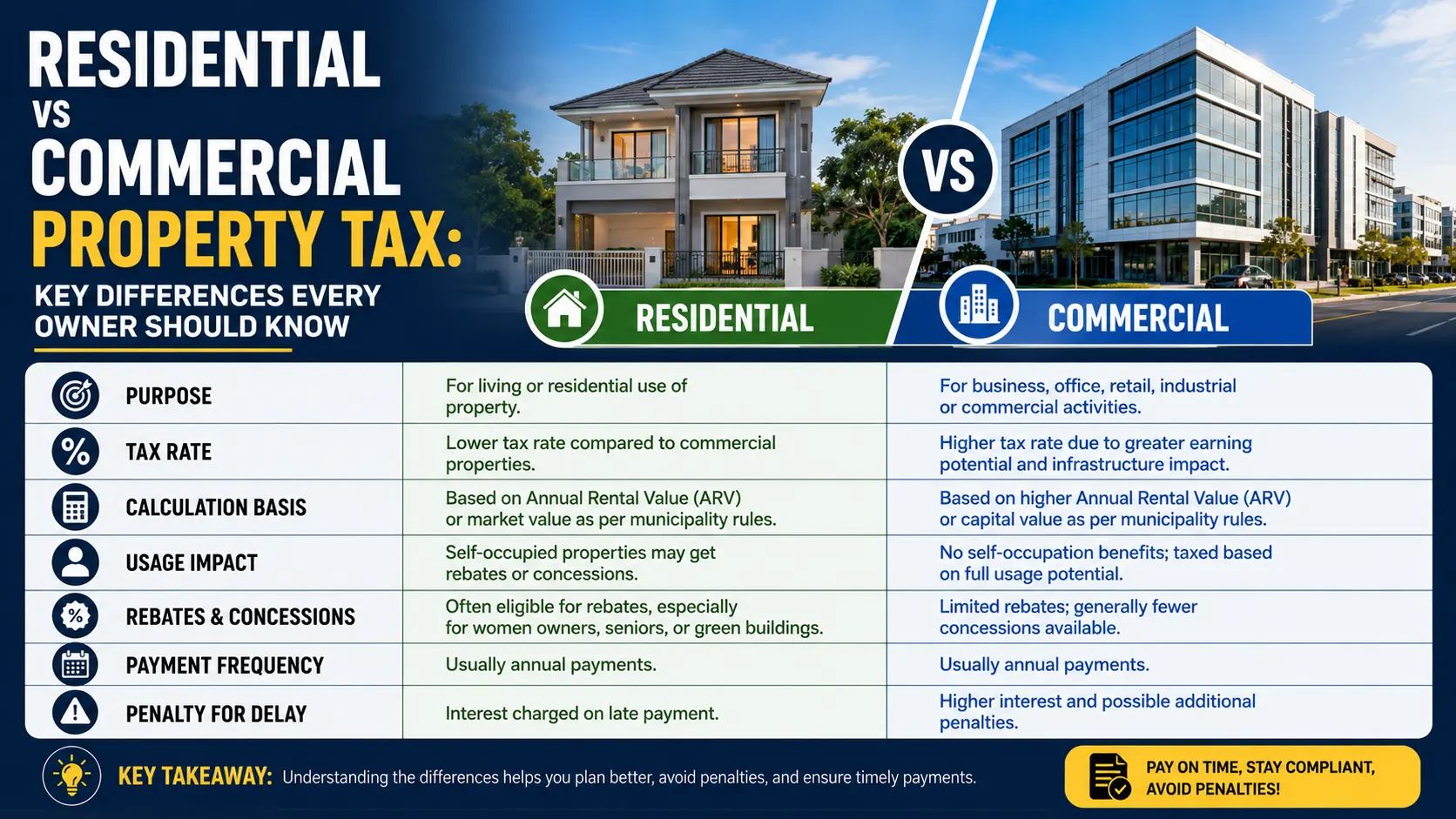

Residential Vs Commercial Property Tax

22, Jun 2026

Boho Chic Interior Design

19, Jun 2026

Scandinavian Interior Design Ideas

17, Jun 2026

How to Design a Beautiful Home on a BudgetPower Shutdown Scheduled Across Several Chennai Areas on Wednesday, Best...

Tamil Nadu’s Economic Momentum Strengthens Real Estate Confidence, Best Builder...

Chennai development body to withdraw from construction, prioritise urban planning,...

Rs 2,000 crore housing project near Pallikaranai Ramsar site stopped...

Tamil Nadu Government Raises Crop Loan Waiver Limit to Rs...

Yes, we offer property management services for landlords who require assistance with managing their rental properties. Our services include finding tenants, collecting rent, handling maintenance issues, and ensuring compliance with legal requirements.

Construction is the process of building, assembling, or erecting structures, infrastructure, or facilities.

Look for designers with experience in projects similar to yours, check their portfolio, and ensure they understand your vision and budget.

Trends vary, but some popular ones include sustainable design, biophilic design (connecting with nature), and minimalist aesthetics.

The borrower receives a lump sum of money from the lender, which is then repaid over time with interest, typically through monthly payments.